![]() Cinram International Income Fund announced its 2010 third quarter and year to date financial results.

Cinram International Income Fund announced its 2010 third quarter and year to date financial results.

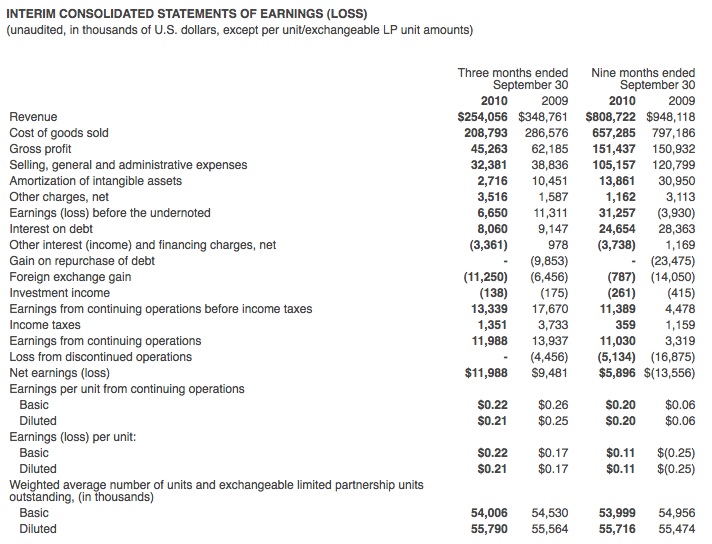

According to the statement, Cinram reported revenue of $254.1 million in the third quarter of 2010 compared to $348.8 million in Q3 2009. Earnings from continuing operations for Q3 2010 was $12.0 million ($0.22/unit basic) compared with $13.9 million ($0.26/unit basic) in Q3 2009.

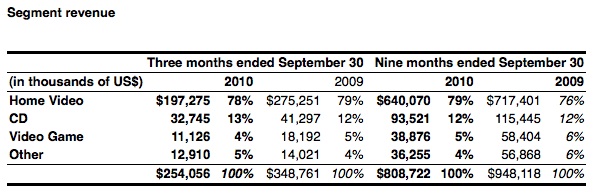

Home video revenue in Q3 2010 fell 28% to $197.3 million from $275.3 million in 2009 and Blu-ray Disc (BD) replication revenue increased to $8.1 million in Q3 2010 from $4.7 million during the same period in 2009.

Cinram trades on the TSX under the symbol CRW.UN

For more information visit: www.cinram.com

Unedited press release follows:

Cinram Reports 2010 Third Quarter Results

(All figures in U.S. dollars unless otherwise indicated)

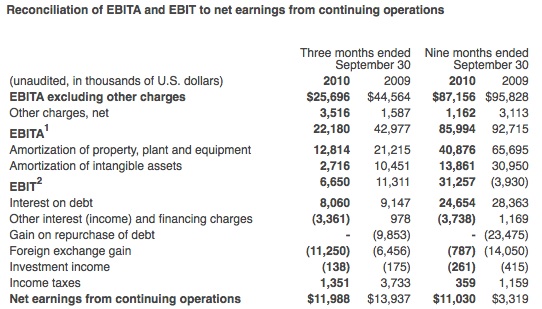

TORONTO, Nov. 2 – Cinram International Income Fund (“Cinram” or the “Fund”) (TSX: CRW.UN) today reported its 2010 third quarter and year to date financial results. The Fund reported revenue of $254.1 million in the 2010 third quarter compared to $348.8 million in the third quarter of 2009. Earnings before interest, taxes and amortization (EBITA1), excluding other charges was $25.7 million compared with $44.6 million in the third quarter of 2009. As a percent of revenue, EBITA excluding other charges was 10.1% in 2010 compared with 12.8% in 2009. As expected, the decrease in revenue and EBITA was primarily the result of the termination of the Warner Home Video (WHV) contract effective July 31, 2010. The Fund reported net income from continuing operations for the 2010 third quarter of $12.0 million or $0.22 per unit (basic) compared with net earnings from continuing operations of $13.9 million or $0.26 per unit (basic) in 2009. On a year to date basis, revenue was $808.7 million compared with $948.1 million in the prior year, while EBITA excluding other charges decreased by 9% to $87.2 million from $95.8 million in 2009.

“The results for the 2010 third quarter were generally above our expectations. While the termination of the Warner Home Video contract became effective July 31, results for the third quarter included a significant amount of WHV offload from our competitor. As anticipated, revenue and EBITA were below prior year levels as a result of the contract loss. However, our margins were better than expected as a result of the ongoing efficiency initiatives,” commented Steve Brown, Chief Executive Officer.

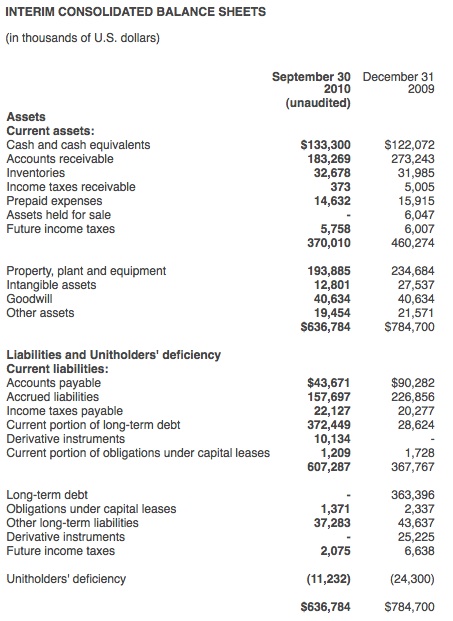

Balance sheet and liquidity

As a result of the maturity of the senior credit facility in May 2011, being less than one year from maturity, the entire debt balance has been recorded as a current liability in our September 30, 2010 balance sheet. As a result, our working capital balance is in a negative position.

“The Company is fully engaged in discussions with its lenders and our respective advisors in a refinancing plan and we expect to make an announcement of the refinancing plan in the near future,” commented John Bell, Chief Financial Officer.

As of September 30, 2010, our net debt position (term debt excluding unamortized transaction costs, less cash and cash equivalents) improved to $240.6 million, compared with $273.3 million at the end of 2009. During the first nine months of 2010, our cash balance increased by $11.2 million to $133.3 million from $122.1 million at the end of 2009.

Third quarter Home Video revenue (which includes replication and distribution of DVDs and Blu-ray discs) was down 28 per cent to $197.3 million from $275.3 million in 2009 as a result of lower DVD unit shipments given the loss of the WHV contract effective July 31st, 2010. Blu-ray disc replication revenue increased to $8.1 million in the third quarter of 2010 from $4.7 million in the comparable 2009 period.

CD segment revenue (which includes replication and distribution of CDs) was down 21 per cent in the third quarter of 2010 to $32.7 million from $41.3 million in 2009 due primarily to lower unit shipments resulting from an expected decline in demand from our CD music label customers.

Video game revenue was $11.1 million in the third quarter of 2010 compared with $18.2 million in 2009 due to continued softness in the gaming industry combined with the loss of several customers.

Revenue from our wireless division related to logistics services was $10.4 million during the third quarter of 2010, compared to $11.1 million in 2009, as the prior year figure includes revenue from the Motorola Europe contract which was terminated effective July 2009.

Geographic revenue

Third quarter North American revenue decreased 29 per cent to $139.6 million from $197.2 million in 2009, principally as a result of lower revenues from the home video, video game distribution and CD segments. North America accounted for 55 per cent of third quarter consolidated revenue compared with 57 percent in the prior year period.

European revenue was down 25 percent in the third quarter to $114.5 million from $151.6 million in 2009. The decrease in revenue was due to several factors including the loss of the WHV business during the third quarter of 2010, combined with the foreign exchange impact associated with a weaker Euro relative to the U.S. dollar during the third quarter of 2010 compared to the same period in the prior year. Excluding the impact of foreign currency translation, European revenue decreased by 18 percent in the 2010 third quarter compared to the prior year period. Third quarter European revenue represented 45 percent of consolidated revenue compared with 43 percent in the third quarter of 2009.

Other financial highlights

Gross profit for the third quarter of 2010 decreased to $45.3 million from $62.2 million in 2009. The Fund recorded amortization expense relating to capital assets (included in the cost of goods sold) of $12.8 million compared to $21.2 million in the third quarter of 2009. This reduction in amortization results from the lower net book value of property, plant and equipment due to impairment charges recorded at the end of 2009 as part of Cinram’s annual impairment test. Excluding capital asset amortization charges, gross profit as a percent of sales was 23 percent in the third quarter of 2010, compared with 24 percent in the prior year period.

Selling, general and administrative expenses decreased in the third quarter of 2010 to $32.4 million from $38.8 million in 2009. As a percentage of consolidated revenues, selling, general and administration expenses were 13 percent compared with 11 percent in 2009.

On June 30, 2010, the Fund completed the sale of its 50% share of the Mexican joint venture, Cinram Latinoamericana, S.A. de C.V, to the joint venture partner for total proceeds of $0.3 million. The agreement includes contingent consideration of up to another $0.2 million should certain conditions be met before the end of 2010. Accordingly, the Funds’ proportionate share of the results of operations of the joint venture were segregated and presented separately as discontinued operations in the consolidated financial statements for the three and nine months ended September 30, 2010, and prior periods have been reflected on this basis.

Unit data

For the three month period ended September 30, 2010, the basic weighted average number of units and exchangeable limited partnership units outstanding was 54.0 million compared with 54.5 million in the prior year. For the nine month period ended September 30, 2010, the basic weighted average number of units and exchangeable limited partnership units outstanding was 54.0 million compared with 55.0 million in the prior year.

1 EBITA is defined as earnings (loss) from continuing operations before interest expense, foreign exchange translation gain/losses, investment income, gain on repurchase of debt, other interest and financing charges, income taxes and amortization. It is a standard measure that is commonly reported and widely used in the industry to assist in understanding and comparing operating results. EBITA is not a defined term under generally accepted accounting principles (GAAP). Accordingly, this measure may not be comparable with other issuers and should not be considered as a substitute or alternative for net earnings or cash flow, in each case as determined in accordance with GAAP. See reconciliation of EBITA to net earnings under GAAP as found in the table above.

2 EBIT is defined as earnings (loss) from continuing operations before interest expense, foreign exchange translation gains/losses, investment income, gain on repurchase of debt, other interest and financing charges and incomes taxes, and is a standard measure that is commonly reported and widely used in the industry to assist in understanding and comparing operating results. EBIT is not a defined term under GAAP. Accordingly, this measure may not be comparable with other issuers and should not be considered as a substitute or alternative for net earnings or cash flow, in each case as determined in accordance with GAAP. See reconciliation of EBIT to net earnings under GAAP as found in the table above.

About Cinram

Cinram International Inc., an indirect, wholly-owned subsidiary of the Fund, is one of the world’s largest providers of pre-recorded multimedia products and related logistics services. With facilities in North America and Europe, Cinram International Inc. manufactures and distributes pre-recorded DVDs, Blu-ray discs, audio CDs, and CD-ROMs for motion picture studios, music labels, publishers and computer software companies around the world. Cinram also provides distribution and logistics services to the telecommunications industry in North America through its wireless subsidiary. The Fund’s units are listed on the Toronto Stock Exchange under the symbol CRW.UN. For more information, visit our website at www.cinram.com.

Certain statements included in this release constitute “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Fund, or results of the multimedia duplication/ replication industry, to be materially different from any future results, performance or achievements expressed or implied by such forward looking statements. Such factors include, among others, the following: the Fund’s ability to retain major customers; general economic and business conditions, which will, among other things, impact the demand for the Fund’s products and services; multimedia replication industry conditions and capacity; the ability of the Fund to implement its business strategy; the Fund’s ability to invest successfully in new technologies and other factors which are described in the Fund’s filings with the securities commissions.