![]() DisplaySearch announced that 2010 was a strong year for plasma TV panel shipments.

DisplaySearch announced that 2010 was a strong year for plasma TV panel shipments.

For more information visit: www.displaysearch.com

Unedited press release follows:

Plasma TV Panel Shipments Hit Record High in Q4’10

Strong Value Proposition Against LED-Backlit LCD TV and Good 3D Performance Boosts Shipments

SANTA CLARA, CALIF., February 3, 2011 — 2010 was a great year for plasma TV panels, with shipments growing Y/Y every quarter since Q4’09. Growth seems to be supply-limited. This is a surprising result, as weak economic conditions resulted in several plasma players exiting the plasma TV business in 2009, and plasma faced a renewed threat from LCD TVs with the improvements from LED backlights narrowing the performance gap with plasma. However, the aggressive rollout of LED-backlit LCD TVs caused a significant slowdown in the decline in LCD TV average prices, and with the increased importance of value in many markets, plasma TV was very competitive with LCD in greater than 40″ market segments.

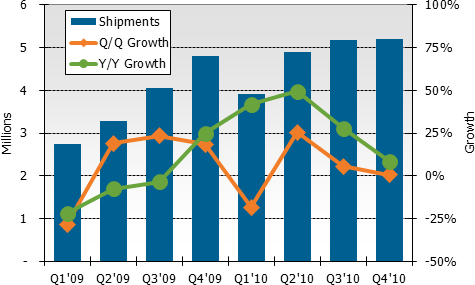

Figure 1: Plasma Panel Shipments by Quarter

Source: Quarterly Global TV Shipment and Forecast Report, Plasma and LCD TV Panel Shipment Module

According to the DisplaySearch Quarterly Global TV Shipment and Forecast Report, Plasma and LCD TV Panel Shipment Module, Q4’10 plasma TV panel shipments grew 1% Q/Q and 9% Y/Y to 5.2M units. Major plasma makers operated at maximum capacity, and one new entrant—COC—started mass production of 42″ panels in China in Q4’10.

Plasma TVs were well-suited for consumers’ purchasing habits in 2010, providing the most affordable large flat panel TVs for many consumers. In addition, the strong industry push for 3D TV helped, as some reviewers and consumers concluded that plasma TV had superior 3D performance compared to LCD TV, at least in terms of flicker.

“While 3D has not played a big role in the growth of plasma shipments, it has helped to support plasma TV in the competition with LCD TV,” noted Ken Park, DisplaySearch Senior Analyst for Korea TV Market Research. “With 3D functionality, plasma can re-position itself as a lasting technology in the TV industry. In fact, plasma TV brands are entering 2011 with 3D across their product portfolios, from 42″HD to 152″.”

The top plasma TV panel suppliers in 2010 on a unit basis were Panasonic, which grew 22% Y/Y, Samsung SDI, which grew 37% Y/Y, and LGE, which grew 30% Y/Y.

Table 1: Plasma Panel Unit Share & Growth by Supplier (2009-2010)

| Rank | Supplier | 2009 Unit Share | 2010 Unit Share | Unit Y/Y | Revenue Y/Y |

| #1 | Panasonic | 43.1% | 40.7% | 22% | 4% |

| #2 | Samsung SDI | 31.7% | 33.7% | 37% | 15% |

| #3 | LGE | 23.1% | 23.3% | 30% | 22% |

| #4 | COC | 0.6% | 2.2% | 421% | 356% |

| Total | 98.4% | 99.9% | 29% | 11% |

Source: Quarterly Global TV Shipment and Forecast Report, Plasma and LCD TV Panel Shipment Module

Additional findings in the DisplaySearch Quarterly Global TV Shipment and Forecast Report, Plasma and LCD TV Panel Shipment Module include the following:

* After falling from 15.1M in 2008 to 14.8M in 2009, plasma TV panel shipments jumped to 19.1M in 2010.

* The share of plasma TV panel shipments at 50”+ reached 40.8% in 2010, up from 38.0% in 2009, as plasma TV panel makers exited the 32” market due to low LCD prices, while the 42” market has narrow profit margins, leading plasma TV brands to focus on the 50”+ market where they remain more competitively priced than LCD.

* The share of plasma TV panel shipments at 1080p barely increased in 2010, as consumers were still price sensitive. Thus, Samsung introduced a 50” 720p 3D plasma TV for the first time in the second half of the year.

For detailed plasma module shipments, plasma fab activity, plasma supply/demand, plasma TV shipments by brand and region, and rolling 16-quarter plasma shipment, cost and pricing forecasts, please see the latest Quarterly Global TV Shipment and Forecast Report, Plasma and LCD TV Panel Shipment Module. Note, DisplaySearch’s comprehensive plasma market data research is available exclusively in the Quarterly Global TV Shipment and Forecast Report.

For more information contact Charles Camaroto at 1.888.436.7673 or 1.516.625.2452, e-mail contact@displaysearch.com, or contact your regional DisplaySearch office in China, Japan, Korea or Taiwan for more information.

About DisplaySearch

Since 1996, DisplaySearch has been recognized as a leading global market research and consulting firm specializing in the display supply chain, as well as the emerging photovoltaic/solar cell industries. DisplaySearch provides trend information, forecasts and analyses developed by a global team of experienced analysts with extensive industry knowledge. In collaboration with the NPD Group, its parent company, DisplaySearch uniquely offers a true end-to-end view of the display supply chain from materials and components to shipments of electronic devices with displays to sales of major consumer and commercial channels. For more information on DisplaySearch analysts, reports and industry events, visit us at www.displaysearch.com. Read our blog at www.displaysearchblog.com and follow us on Twitter at @DisplaySearch.

About The NPD Group, Inc.

The NPD Group is the leading provider of reliable and comprehensive consumer and retail information for a wide range of industries. Today, more than 1,800 manufacturers, retailers, and service companies rely on NPD to help them drive critical business decisions at the global, national, and local market levels. NPD helps our clients to identify new business opportunities and guide product development, marketing, sales, merchandising, and other functions. Information is available for the following industry sectors: automotive, beauty, commercial technology, consumer technology, entertainment, fashion, food and beverage, foodservice, home, office supplies, software, sports, toys, and wireless. For more information, contact us or visit www.npd.com and http://www.npdgroupblog.com/. Follow us on Twitter at @npdtech and @npdgroup.