![]() NPD DisplaySearch announced it forecasts that worldwide LCD TV shipments will rise from 206 million units in 2011 to 225 million units in 2012.

NPD DisplaySearch announced it forecasts that worldwide LCD TV shipments will rise from 206 million units in 2011 to 225 million units in 2012.

For more information visit: www.displaysearch.com

Unedited press release follows:

LCD TV Shipment Growth to Improve in 2012, Driven by 40” and Larger Sizes

Total TV Market to Rise 2% in 2012 After No Growth in 2011 Due to Soft Consumer Demand and Early Inventory Pressure, NPD DisplaySearch Reports

SANTA CLARA, Calif., January 3, 2012—Consumer demand for TVs has been softer than expected in 2011, but showing signs of improvement late in the year. However, inventory pressure plagued the industry through much of early 2011 and led to a sharp reduction in shipments to retailers. The result is that global TV unit shipments are expected to rise only 0.1% in 2011. According to the latest forecast released in the NPD DisplaySearch Advanced Quarterly Global TV Shipment and Forecast Report, growth is expected to improve in 2012, rising 2% to 254 million units.

“Global economic conditions have improved in 2011, but more slowly than expected, and consumers in mature TV markets like Europe face continuing uncertainty, which is leading to very cautious spending patterns,” noted Paul Gagnon, Director of North America TV Research for NPD DisplaySearch. Gagnon added, “Because price reductions are not as vigorous as a few years ago, partially due to a mature manufacturing base but also because of transitions to advanced features like LED backlights and 3D, consumers are becoming more willing to wait for peak sale periods to purchase.”

Flat panel TV continues to grow, but at a more gradual pace of 2-4% per year as the rapid transition from CRT to LCD and plasma nears an end. LCD TV continues to be the dominant technology on a unit and revenue basis, and in fact seems likely capture even more market share due to a weaker outlook for plasma TV going forward. As LCD narrows the pricing gap with plasma at many sizes, the demand for plasma has fallen; NPD DisplaySearch expects this to continue and has reduced its forecast for plasma TV.

Large TV sizes also continue to show strong growth, with shipments of 40”+ and larger sets expected to grow 12% in 2012 while <40” sizes decline 3%. A strong contributing factor to the growth of larger sizes, including an 18% increase in shipments of 50”+ sets, is pricing. Sizes up to 50” will have average prices below $1000 in 2012 and even 60”+ sizes will fall below $2000 for the first time. During Black Friday holiday sales in the US, many 40-47” sets were below $500, and even 60” sets fell below $1000, prompting robust unit sales as consumers were attracted to the new price points. Many consumers seem to be willing to give up features in favor of larger sizes for a given TV buying budget. Even in China, shipment share of 50”+ and larger sizes is growing strongly and may become the only region outside of North America to reach 10% 50”+ mix of unit shipments by 2015.

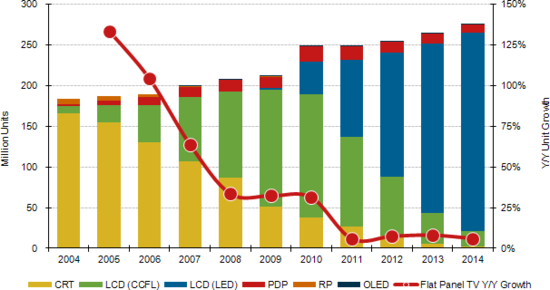

Figure 1: Worldwide TV Forecast by Technology

Source: NPD DisplaySearch Advanced Quarterly Global TV Shipment and Forecast Report

LCD TV Will Remain the #1 TV Technology with LED Share Reaching 67% in 2012

LCD TV shipments will rise from 206M units in 2011 to 225M units in 2012, an increase of 9%. LCD will account for more than 82% of all global TV shipments in 2011, rising to more than 88% in 2012, as demand for plasma falls and OLED TVs arrive late in the year in small quantities and at high prices. LCD is now a strong competitive technology at all sizes and should climb to more than 95% share by 2014 as CRT fades and OLED is slow to grow.

Premium features continue to grow, like LED backlights and 3D, and are keeping LCD TV average prices very stable, falling just 6% Y/Y on a volume weighted basis in 2011, the slowest year of LCD TV price erosion yet. Price erosion will be about the same in 2012 before picking up to 7-8% per year through 2015, but much less than the 24% decline seen in 2009. However, with the slower ASP erosion, total LCD TV revenue growth should remain positive through 2013 at 1-3% per year. The share of LED backlights in LCD TV shipments is expected to be about 46% in 2011, rising to nearly 68% in 2012. 3D will account for around 3% of LCD TV units this year.

Plasma TV units grew 30% in 2010 due to a favorable pricing advantage over LCD, but as that advantage has narrowed in 2011, shipments are expected to fall 11%, to 16.3 million units. The decline in unit growth and weak profits have led manufacturers to focus on more profitable segments, even at the expense of unit growth. As a result, plasma TV shipments are projected to fall to less than 10 million units by 2015.

The first OLED TV shipments are expected in the second half of 2012, but due to prices that are expected to be well above $4000 initially and remain significantly higher than mainstream high-end LCD TVs, will only grow to about 2.5% of the 40”+ segment by 2015.

The worldwide forecast for 3D TVs was slightly increased to more than 23M units in 2011 through better than expected growth in emerging markets and Europe. By contrast, demand in North America has been surprisingly soft for 3D, and may only reach 3.6 million units in 2011 as US consumers remain very price sensitive. Eventually though, North America will see a rise in 3D adoption due to stronger preference for 40”+ sizes where the 3D feature is common and expected to be less costly. Globally, 3D TV is expected rise to more than 100M units shipped by 2015.

Emerging regions, which includes China, Asia Pacific, Latin America, Eastern Europe, and Middle East / Africa, will account for the majority of flat panel TV growth over the next four years, averaging 11% growth each year, while developed regions decline an average of 1% each year. In fact, China has become the largest market for flat panel TVs and will continue to be throughout the forecast period. The Asia Pacific region is positioned for strongest growth as the late-adopting India market begins to boom.

The NPD DisplaySearch Q4’11 Advanced Quarterly Global TV Shipment and Forecast Report includes panel and TV shipments by region and by size for nearly 60 brands, and also includes rolling 16-quarter forecasts, TV cost/price forecasts and design wins. This report is delivered in PowerPoint and includes Excel-based data and tables. If you need further information or assistance please contact us at +1.408.418.1900 or sales@displaysearch.com or at the local DisplaySearch offices in China, Japan, Korea, Taiwan and the United Kingdom.

For more information on this report, please contact Charles Camaroto at 1.888.436.7673 or 1.516.625.2452, or contact@displaysearch.com or contact your regional DisplaySearch office in China, Japan, Korea or Taiwan.

About NPD DisplaySearch

Since 1996, NPD DisplaySearch has been recognized as a leading global market research and consulting firm specializing in the display supply chain, as well as the emerging photovoltaic/solar cell industries. NPD DisplaySearch provides trend information, forecasts and analyses developed by a global team of experienced analysts with extensive industry knowledge and resources. In collaboration with The NPD Group, its parent company, NPD DisplaySearch uniquely offers a true end-to-end view of the display supply chain from materials and components to shipments of electronic devices with displays to sales of major consumer and commercial channels. For more information on NPD DisplaySearch analysts, reports and industry events, visit us at http://www.displaysearch.com/. Read our blog at http://www.displaysearchblog.com/ and follow us on Twitter at @DisplaySearch.

About The NPD Group, Inc.

The NPD Group is the leading provider of reliable and comprehensive consumer and retail information for a wide range of industries. Today, more than 1,800 manufacturers, retailers, and service companies rely on NPD to help them drive critical business decisions at the global, national, and local market levels. NPD helps our clients to identify new business opportunities and guide product development, marketing, sales, merchandising, and other functions. Information is available for the following industry sectors: automotive, beauty, commercial technology, consumer technology, entertainment, fashion, food and beverage, foodservice, home, office supplies, software, sports, toys, and wireless. For more information, contact us or visit http://www.npd.com/ and http://www.npdgroupblog.com/. Follow us on Twitter at @npdtech and @npdgroup.