![]() DisplaySearch announced that, according to its research, mobile phone display shipments were 413.2 million units in the third quarter of 2010 with revenues reaching $3.38 billion.

DisplaySearch announced that, according to its research, mobile phone display shipments were 413.2 million units in the third quarter of 2010 with revenues reaching $3.38 billion.

For more information visit: www.displaysearch.com

Unedited press release follows:

Mobile Phone Display Shortages and New Technologies Result in Higher Prices

Strong Growth for AMOLED in Smart Phones from Nokia and Samsung, up 65% in Q3’10 and 132% Y/Y

Santa Clara, California, February 23, 2011 — As the mobile phone industry focuses on touch-enabled smart phones, results from the DisplaySearch Quarterly Mobile Phone Shipment and Forecast Report indicate strong revenue and shipment growth for this segment in Q3’10. Mobile phone display shipments were 413.2 Million in Q3’10, up 6% Q/Q. Revenues for this segment grew even faster, at 13% Q/Q, to reach $3.38 billion. This was the third consecutive quarter that revenue growth outpaced shipment growth.

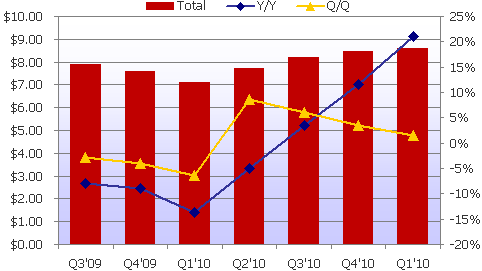

“In Q3, we saw critical changes in key specifications of mobile phone displays, such as size and technology. This influenced the ASP for mobile phone displays, which was $8.19 in Q3’10, up 4% Y/Y and 6% Q/Q. Despite this, ASPs for each size or specification continued to fall as usual,” noted Calvin Hsieh, Senior Analyst at DisplaySearch. “Increased demand for upgraded specifications (such as display size, technology, and resolution), and a shift in display technologies used in mobile phones compensated for falling ASPs—resulting in strong revenue growth.”

Figure 1. Average Selling Prices for Mobile Phone Displays

Source: DisplaySearch Quarterly Mobile Phone Shipment and Forecast Report

Higher Display Resolution Driven by Smart Phones

Demand for higher resolution displays (320×480/HVGA or higher) reached 22.5% in Q3’10. In particular, the share of WVGA (400×800 and 400×864) resolution increased to 8%, compared to 3.5% in Q1’10 and 5.3% in Q2’10. DVGA (640×960) resolution displays, such as Apple’s retina display, also grew, to 3.2% from 1.9% in Q2’10.

AMOLED Growing Share

Samsung and Nokia have been increasing the use of AMOLED displays in their mobile phones. As a result, Q3’10 shipments reached 13.5M, up 132% Y/Y and 65% Q/Q. For the first time, AMOLED revenue share passed 10% (10.7%, up from 6.4% in Q2’10). AMOLED displays have been particularly successful in smart phones; for example, 4”, 480×800 resolution displays (which accounted for 81% (11M) of AMOLED shipments) were used in Samsung’s Galaxy S i9000. Samsung Mobile Display (SMD) had 98.3% share of AMOLED panels in mobile phones in Q3’10.

A-Si TFT LCD Continues to Lead

While AMOLED and LTPS TFT LCD are increasing their share of the mobile phone display market, increased demand for larger sizes and higher resolutions has allowed mainstream a-Si TFT LCD to maintain a 60% share of mobile phone display shipments, followed by LTPS TFT LCD, which increased its share to 22.5%.

Using detailed supplier surveys, DisplaySearch examines shipment, revenue, and pricing data by key metrics for small/medium displays, including market application, size, resolution, technology and supplier. Available research includes four quarterly reports focusing on different aspects of the market. The comprehensive Quarterly Small/Medium Shipment and Forecast Report provides full market analysis while the Quarterly Small/Medium Pricing Report, Quarterly Mobile Phone Shipment and Forecast Report and Quarterly Small/Medium Value Chain Report focus on ASPs, mobile phone displays, and market share data, respectively. For more information contact Charles Camaroto at 1.888.436.7673 or 1.516.625.2452, e-mail contact@displaysearch.com, or contact your regional DisplaySearch office in China, Japan, Korea or Taiwan for more information.

About DisplaySearch

Since 1996, DisplaySearch has been recognized as a leading global market research and consulting firm specializing in the display supply chain, as well as the emerging photovoltaic/solar cell industries. DisplaySearch provides trend information, forecasts and analyses developed by a global team of experienced analysts with extensive industry knowledge. In collaboration with the NPD Group, its parent company, DisplaySearch uniquely offers a true end-to-end view of the display supply chain from materials and components to shipments of electronic devices with displays to sales of major consumer and commercial channels. For more information on DisplaySearch analysts, reports and industry events, visit us at http://www.displaysearch.com/. Read our blog at http://www.displaysearchblog.com/ and follow us on Twitter at @DisplaySearch.

About The NPD Group, Inc.

The NPD Group is the leading provider of reliable and comprehensive consumer and retail information for a wide range of industries. Today, more than 1,800 manufacturers, retailers, and service companies rely on NPD to help them drive critical business decisions at the global, national, and local market levels. NPD helps our clients to identify new business opportunities and guide product development, marketing, sales, merchandising, and other functions. Information is available for the following industry sectors: automotive, beauty, commercial technology, consumer technology, entertainment, fashion, food and beverage, foodservice, home, office supplies, software, sports, toys, and wireless. For more information, contact us or visit http://www.npd.com/ and http://www.npdgroupblog.com/. Follow us on Twitter at @npdtech and @npdgroup.