IHS Screen Digest announced it reckons that the number of U.S. households subscribing to pay television video services declined by nearly 370,000 in the second quarter of 2011, with cable operators taking the biggest hit.

IHS Screen Digest announced it reckons that the number of U.S. households subscribing to pay television video services declined by nearly 370,000 in the second quarter of 2011, with cable operators taking the biggest hit.

For more information visit: www.isuppli.com

Unedited press release follows

Cutting Through the Cord-Cutting Hype: US Pay-TV Market Shows Resilience in Q2

El Segundo, Calif., September 9, 2011—Despite a decline in video subscribers, the second quarter actually was a strong period for the U.S. pay-TV business, with revenue-generating units (RGU) for cable rising robustly due to the expanding broadband and telephony segments, according to new IHS Screen Digest U.S. Cable Networks Intelligence research findings from information and analysis provider IHS (NYSE: IHS).

The number of U.S. households subscribing to pay television video services declined by a total of nearly 370,000 in the second quarter, with cable operators taking the biggest hit. However, total cable RGUs, or individual service subscriber contracts, actually rose by 238,000 on the strength of increased subscriptions for non-video services.

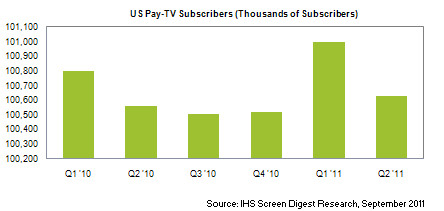

Total U.S. pay-TV video subscriptions in the second quarter decreased to 100.6 million, down from 101 million in the first quarter, as presented in Figure 1 below. These numbers encompass subscribers in three areas of the pay-TV video business: cable, satellite video and Internet Protocol TV (IPTV) services provided by telcos.

The decrease represented only the third time in history that the U.S. pay-TV video market has suffered a sequential quarterly decline. The previous market contractions occurred in the second and third quarters of 2010.

However, the second-quarter decline comes after a 13,000 increase in video subscribers that occurred in the fourth quarter of 2010 and a 477,000 gain during the first quarter of this year. This means that total U.S. pay-TV video subscribers in the second quarter of 2011 actually were slightly higher than they were one year earlier, up by about 68,000 compared to the second quarter of 2010.

“This seesaw pattern of quarterly growth and decline is indicative of a mature industry that has reached a high level of saturation, with subscription video services now being sold to some 85 percent of all U.S. homes,” said Erik Brannon, analyst for U.S. Cable Network Intelligence and U.S. TV Intelligence at IHS. “Like any mature industry in a recession, the video side of the business is seeing some softness, but not the kind of steady or accelerating drops one would expect if—as some are suggesting—the American consumer is abandoning pay-TV en masse in favor of Internet-delivered video, a phenomenon known as ‘cord cutting.’ This indicates that the threat of cord-cutting has been overblown.”

Cable’s silver lining

For U.S. cable providers, the loss of business in their traditional video-services stronghold is not the whole story. While significant declines in video subscriptions are taking their toll, cable companies are recouping their losses by signing up high-speed data (HSD) and voice-over-Internet-protocol (VOIP) service subscribers at a faster rate than they are losing video subscribers, thereby growing their RGU counts, as presented in the figure below.

During the second quarter, U.S. cable operators posted gains of 270,000 broadband subscribers and 593,000 VOIP subscribers. This more than offset the loss of 625,000 video subscribers, and left 59.3 million households still subscribing to cable video services.

At the same time, IHS expects that as the economy pulls out of its current recessionary trends, many former subscribers will re-enroll for video service. But even in a worst-case scenario where cable loses 10 percent of its video subscriber base by 2015, operators will maintain noteworthy operating margins thanks to their cash-flow-rich HSD and VOIP services.

Satellite shares the pain, IPTV still growing

The U.S. satellite video sector, populated by DISH Network and DirecTV, also saw the flight of some 109,000 subscribers during the second quarter, bringing the total down to 33.5 million. DirecTV undoubtedly has been successful at capturing the high end of the market with its sports packages, while DISH Network has built its business on the back of cost-conscious consumers. Nonetheless, both face pressure from the declining demand for video packages, and neither has the infrastructure in place to independently offer HSD or VOIP.

The only sector to post video-subscriber gains in the second quarter was IPTV, thanks to the strong performances of its biggest two players, Verizon FiOS and AT&T U-verse. The two companies’ U.S. subscriber numbers collectively reached 7.9 million, a net addition of 366,000. Underpenetrated at the moment, the IPTV segment is in the strongest position among the three video-providers going forward, with IHS predicting a 7.2 percent compound annual growth rate in the United States through 2015.

Pay-TV versus the Internet

“The threat of consumers discontinuing video service in favor of the Internet must be viewed in the context of the current economic environment,” Brannon noted. “In better times, subscribers were happy to pay for both video subscriptions and for high-speed Internet subscriptions, as evidence by the rapid growth in both in the pre-2008 period. In the current economic situation, when forced to choose, some consumers appear to see greater value in the latter. But given the high percentage of people who are unemployed or underemployed, IHS believes that the relative stability of sub-counts—especially at the RGU level—is testimony to the value that consumers see in pay-TV services.”

To learn more, see IHS Screen Digest U.S.Cable Networks Intelligence.

About IHS(www.ihs.com)

IHS (NYSE: IHS) is the leading source of information and insight in critical areas that shape today’s business landscape, including energy and power; design and supply chain; defense, risk and security; environmental, health and safety (EHS) and sustainability; country and industry forecasting; and commodities, pricing and cost. Businesses and governments in more than 165 countries around the globe rely on the comprehensive content, expert independent analysis and flexible delivery methods of IHS to make high-impact decisions and develop strategies with speed and confidence. IHS has been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, IHS employs more than 5,100 people in more than 30 countries around the world.