![]() Gartner, Inc. announced it reckons that worldwide PC shipments totalled 87.5 million units in the second quarter of 2012, a decline of 0.1% from the same time last year.

Gartner, Inc. announced it reckons that worldwide PC shipments totalled 87.5 million units in the second quarter of 2012, a decline of 0.1% from the same time last year.

For more information visit: www.gartner.com

Unedited press release follows:

Gartner Says Worldwide PC Shipment Growth Was Flat in Second Quarter of 2012

Ultrabooks Had Little Impact on Overall Shipments in the Quarter

STAMFORD, Conn., July 11, 2012— Worldwide PC shipments totaled 87.5 million units in the second quarter of 2012, a decline of 0.1 percent from the second quarter of 2011, according to preliminary results by Gartner, Inc.

“In the second quarter of 2012, the PC market suffered through its seventh consecutive quarter of flat to single-digit growth,” said Mikako Kitagawa, principal analyst at Gartner. “Uncertainties in the economy in various regions, as well as consumer’s low interest in PC purchases, were some of the key influencers of slow PC shipment growth. Despite the high expectations for the thin and light notebook segment, Ultrabooks, shipment volume was small and little impact on overall shipment growth.”

“Consumers are less interested in spending on PCs as there are other technology product and services, such as the latest smartphones and media tablets that they are purchasing. This is more of a trend in the mature market as PCs are highly saturated in these markets,” Ms. Kitagawa said. “A big portion of R&D spending has been allocated to Ultrabook development, together with Intel’s massive investments to establish the market segment. Though Ultrabook was at first introduced in the market in 2011, the major promotion kicked off toward the end of 2Q12 with the IvyBridge, based Ultrabook release. This segment is still in an early adopter’s stage.”

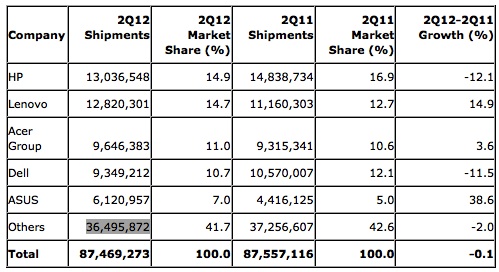

HP continued to be in the top position in worldwide PC shipments (see Table 1). It accounted for 14.9 percent of the market, but its global shipments declined 12.1 percent. Some of HP’s disappointing results were due to internal issues from the organizational changes. HP’s PC business has not been back to pre re-structuring level yet. The company also faced aggressive pricing from Lenovo in the professional market, and threats from companies such as ASUS and Samsung in the already crowded consumer markets.

Table 1

Preliminary Worldwide PC Vendor Unit Shipment Estimates for 2Q12 (Units)

Note: Data includes desk-based PCs and mobile PCs, including mini-notebooks but not media tablets such as the iPad.

Source: Gartner (July 2012)

Lenovo’ s shipment growth continued to exceed the worldwide average, significantly narrowing the market share gap with HP. Lenovo has been very aggressive to expand through a series of acquisitions, as well as aggressive pricing. Lenovo’s aggressive expansion damaged its competitor’s performance, namely HP and Dell, by taking shares from them. Lenovo showed significant growth in EMEA though there is growing concern of the inventory build toward the second half of 2012.

Acer managed to increase shipments compared to a year ago, and the company was able to clear its inventory issues, and prepare for the growth. Acer has been one of the first vendors to release Ultrabooks, and it will most likely lower the Ultrabook price faster than other vendors. Acer has been also very actively promoting its media tablet products.

Dell has been in a process of transforming itself from a PC supplier to solution provider for professional markets. Although Dell’s focus was not to pursue the market share gain, Dell needs to maintain certain level of market share. Dell showed year on year shipment decline across all regions, but EMEA and Asia/Pacific were particularly challenging markets.

ASUS showed the strongest growth among the top 5 vendors worldwide, as its shipments increased 38.6 percent in the second quarter of 2012. ASUS’s strong growth came from EMEA and U.S. markets. ASUS did well at diversifying the product portfolio: starting with mini-notebook expansion, then quickly moving to the mid- to high-end notebook market.

In the U.S., PC shipments totaled 15.9 million units in the second quarter of 2012, a 5.7 percent decline from the same period last year. The slowdown in the U.S. market was largely attributed to weak consumer spending on PCs. This reflects a combination of consumers’ reduced interest in PCs, and vendors reduced willingness to sell PCs due to other products and services that consumers are interested. The major promotion of Ultrabooks could potentially change the market dynamics.

“Weakness in the U.S. public market affected the professional segment despite the high PC procurement season in the second quarter,” Ms. Kitagawa said. “Both government and education institutions are encountering tight budget situations. Shipments to the public sector are expected to be lower than normal seasonality.”

HP continued to lead the U.S. PC market, as it accounted for 25 percent of PC shipments in the second quarter of 2012. Among the top 5 vendors in the U.S. PC market, all but Apple experienced a decline in shipments (see Table 2).

Table 2

Preliminary U.S. PC Vendor Unit Shipment Estimates for 2Q12 (Units)

Note: Data includes desk-based PCs and mobile PCs, including mini-notebooks but not media tablets such as the iPad.

Source: Gartner (July 2012)

From a regional perspective, EMEA, Asia/Pacific and Japan registered low single digit-growth while all Americas markets posted year-over-year shipment declines.

PC shipments in EMEA totaled 25.1 million units in the second quarter of 2012, a 1.9 percent increase from the same period last year. Western Europe saw very weak demand across all countries but especially Southern Europe. Consumer willingness to spend on PCs was furthered hindered by the growing eurozone economic crisis. Retailers again took a risk adverse approach but distributors may well have greater levels of inventory. This will hinder future growth of markets as Windows 8 and more Ultramobile notebooks arrive in the second half of 2012.

The Asia/Pacific PC market grew 2 percent, as shipments reached 31.8 million units. The weak U.S. and European economic situation, coupled with the slowing economy in China, affected the region’s market sentiments where people reacted by scaling back on spending due to the uncertainties. There was the tightening of budgets in the professional segment, as well as a lack in new government initiatives to stimulate IT purchasing activities. Consumers either spent on alternative devices or remained cautious on discretionary spending.

In Latin America, PC shipments in the second quarter of 2012 totaled 9.3 million units, a decline of 1.7 percent from the second quarter of last year. PC shipments in Japan grew 2 percent in the second quarter of 2012, as shipments surpassed 3.9 million units.

These results are preliminary. Final statistics will be available soon to clients of Gartner’s PC Quarterly Statistics Worldwide by Region program. This program offers a comprehensive and timely picture of the worldwide PC market, allowing product planning, distribution, marketing and sales organizations to keep abreast of key issues and their future implications around the globe. Additional research can be found on Gartner’s Computing Hardware section on Gartner’s website at http://www.gartner.com/it/products/research/asset_129157_2395.jsp.